PIMS

Proposal Input Management System (PIMS) is a web based data entry system for financial products. Initially designed for the capture of automotive loans PIMS can also be used for fixed and variable rate personal loans.

The following are just some of the features available:

Data Entry

- Secure login for your brokers and or dealers where each broker can only see deals that they have initiated.

- Proposal matching and linking; should a match occur you define how it should be processed eg automatically declined or decision copied from matched proposal. The user also has the option to copy data from a linked proposal to reduce the time for initial data entry.

- Easy to follow wizard for new proposals or data can be entered through the hierarchical tree view.

- Loan details can be entered prior to underwriting or be locked until a decision is made saving brokers time if the proposer is unsuitable.

- Postcode and bank account validation using 3rd party software.

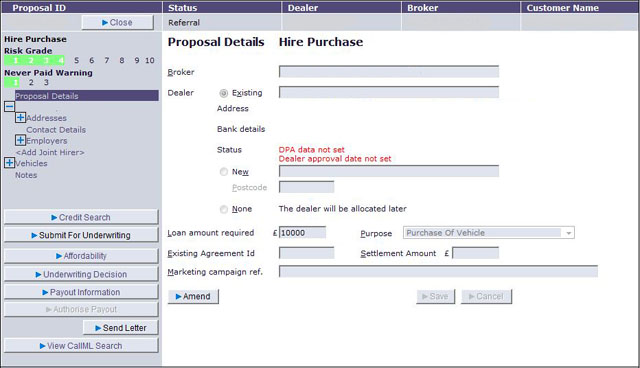

Proposal Details

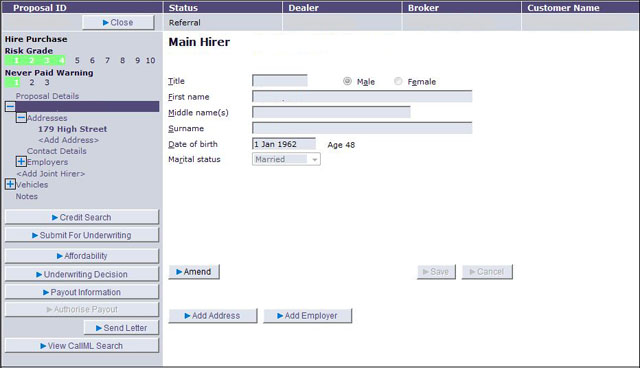

Personal Details

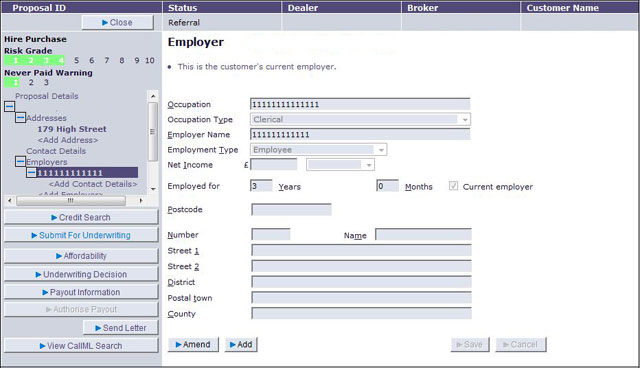

Employer Details

Underwriting

- Basic data checks are made prior to submission to the underwriting process eg minimum address / employment history.

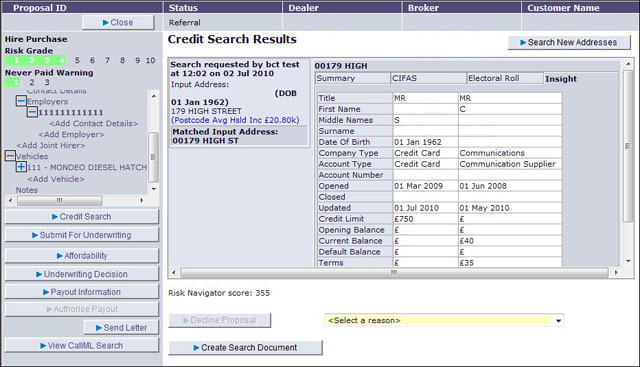

- XML Interface to Equifax credit search bureau to validate customer data prior to underwriting and to provide proposer’s credit data to underwriting process.

- QCB data can also be returned to your requirements and used in underwriting process.

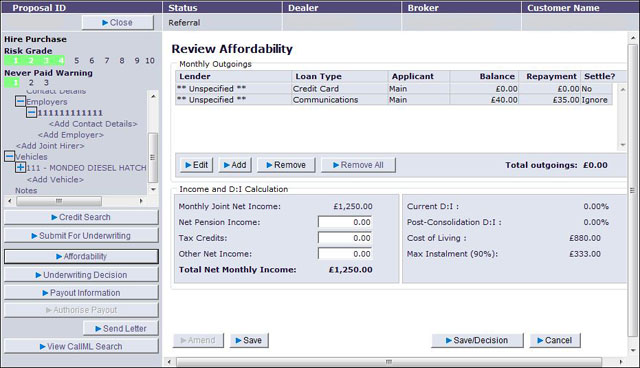

- Dedicated affordability screen for underwriters to evaluate the proposer’s income and expenditure the results can also be incorporated in any automatic decision making.

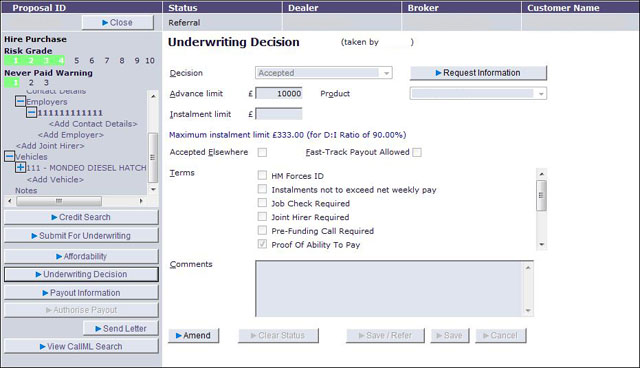

- Underwriting process can be fully automated (based on credit search results and proposal details), manual or a combination of both.

- Business specific criteria checks are implemented to save underwriters manually searching and analysing credit search data for key variables.

- Where CIFAS markers are present on an account then these are only visible to authorised users. Once a non authorised user makes a decision on a proposal this is raised as a reminder to the relevant personnel to review and act accordingly.

- Scorecards are used to analyse specific credit search data and provide underwriters with predefined result sets to ensure a more consistent and less timing consuming underwriting process. The results of the scorecard analysis can also be used within the automatic underwriting process. The scorecard design is flexible and thus only a short lead time is required to implement the rules you require.

Affordability Details

Credit Search Results

Decision Making

- Assuming a proposal is accepted the system or underwriter can specify a number of configurable conditions that have to be met prior to the proposal going live.

- It is possible for an underwriter to refer a decision to a more senior colleague for approval prior to the broker being informed.

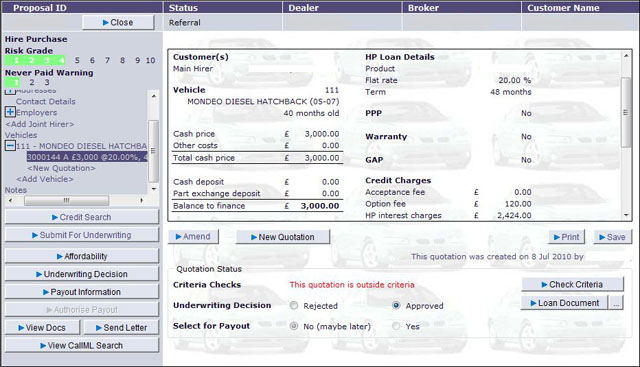

Loan Details

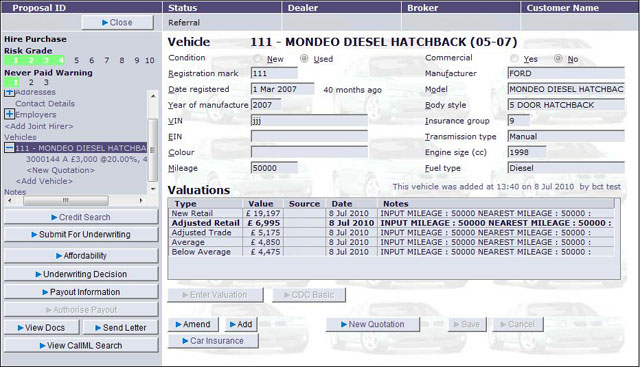

- Vehicles can be loaded either with a registration plate and Experian Car Data Check Lookup or via CAP or Glass’s Guide lookups.

- Current vehicle valuations are retrieved from your preferred supplier.

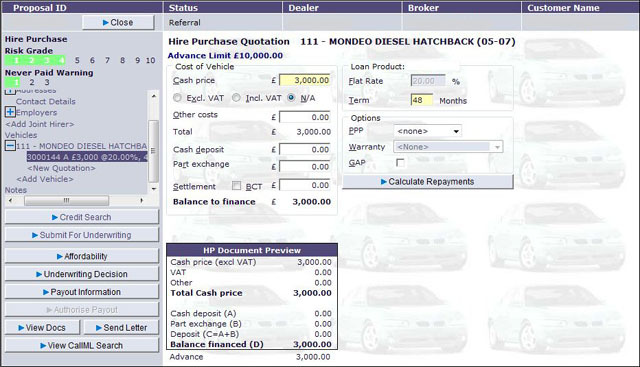

- Following successful data input the loan is calculated according to the product parameters and results displayed to the user. Any commissions payable are also displayed or if the broker prefers hidden in case he is with a client!

Vehicle Details

Quotation Input

Quotation Results

Document Generation

- Loan documentation is generated by the system with all relevant details pre-filled. The documents are stored centrally using our document management system and presented to the broker in PDF format.

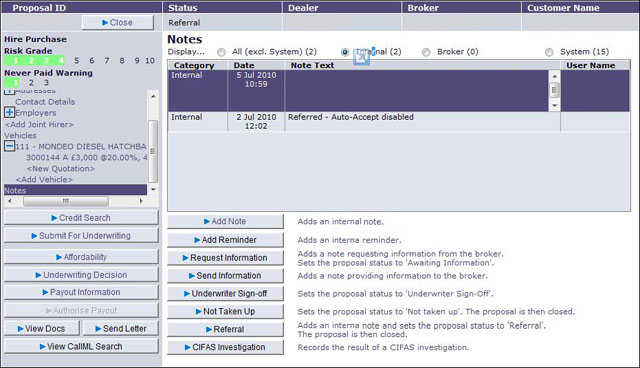

Notes and Reminders

- All parties can apply notes to a proposal at any time. The notes are categorised and access is restricted to appropriate parties for example a broker can only see notes added by you that you wish them to see.

- In addition to notes, users and the system can add reminders to a proposal to ensure specific actions are carried out at the appropriate time. Brokers can submit questions to you on a proposal and these are flagged up as reminders. All reminders are made available through our Queues application.

Configuration

- There are numerous areas within PIMS that can be tailored to your needs eg which products are available by broker or by credit score and for automotive loans the loan to value based on car age, mileage etc.

Message Centre

- Brokers can be sent decisions and requests for further information and these appear in a dedicated message area which appears below the search results on the broker homepage.

Permissions

- These can be applied to tailor access to certain areas, allow inputs by authorised users only and allow users to override base validation plus many more.

Callcredit - CallML

- PIMS also has an interface into Callcredit's money laundering service CallML. Checks are carried out after document are produced and any issues arising from the results are relayed to brokers and users for further checking.

PIMS XML interface

- The interface provides access to many of the key features of PIMS including:

- Loading proposal data, this can be done in a single operation or via multiple calls eg you may load basic proposer details and then later load vehicle details as they come to hand.

- Proposals can be submitted automatically to the underwriting process after loading or held as a new proposal until the broker manually reviews and submits the proposal through the user interface.

- Ability to retrieve full or partial proposal details to check for new decisions and notes from your users.

- Request document production when a proposal has been accepted and suitable loan details entered.